Understanding how financial markets respond to important events is essential for investors, researchers, and business professionals. One of the most widely used methods for measuring market reactions is cumulative abnormal return calculation. This financial concept helps determine whether a company’s stock performs better or worse than expected during a specific event, such as an earnings announcement, merger, product launch, or regulatory decision. By comparing actual returns with expected returns over a defined period, analysts can evaluate the true impact of an event on shareholder value. Learning this concept improves investment analysis, academic research, and financial decision-making.

What Is Cumulative Abnormal Return Calculation?

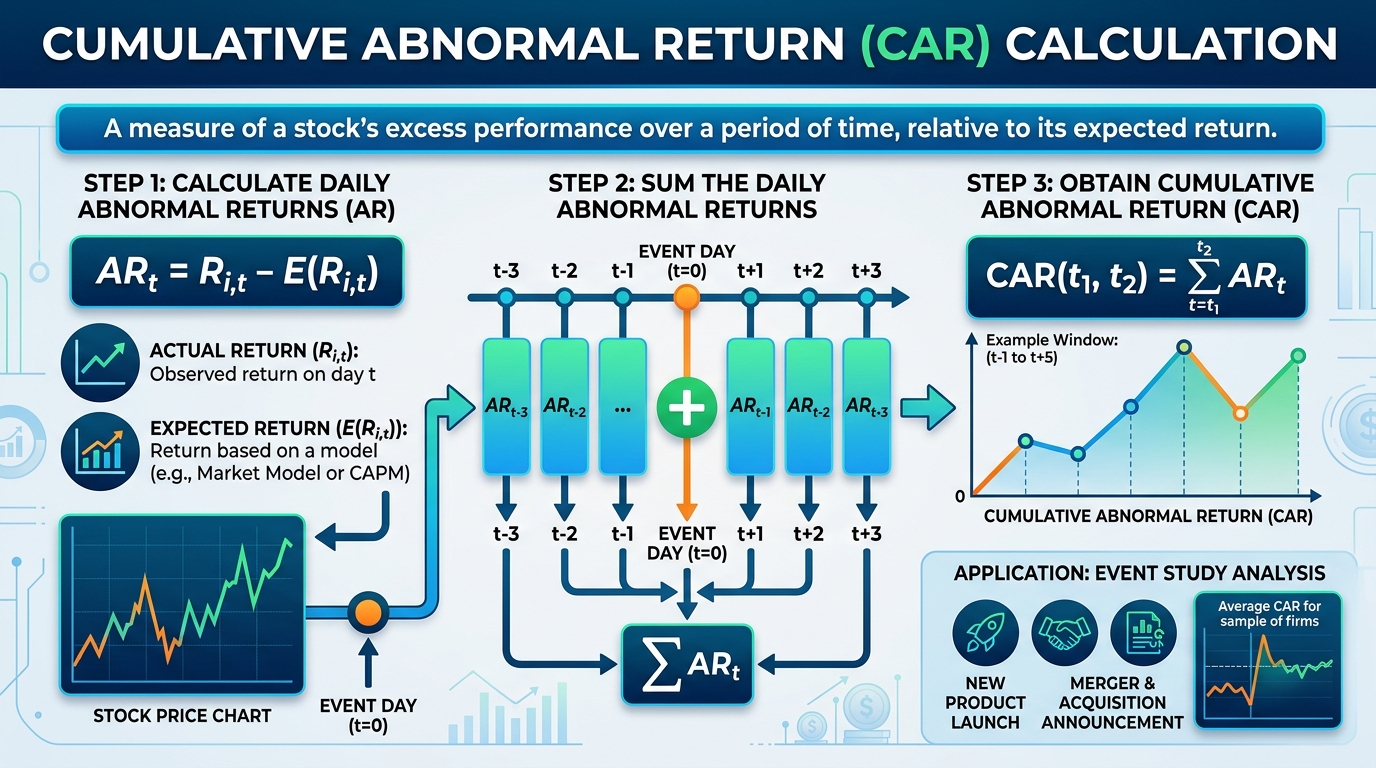

Cumulative abnormal return calculation refers to the process of measuring the total abnormal return generated by a stock over a selected event window. An abnormal return is the difference between a stock’s actual return and its expected return based on market performance or a financial model. When these abnormal returns are added together across several trading days, the result is called cumulative abnormal return, often abbreviated as CAR. This measurement helps analysts determine whether a specific event created positive or negative value for investors. It is widely used in finance, economics, and academic studies involving stock market behavior.

Understanding Abnormal Returns Before Calculating CAR

Before performing cumulative abnormal return calculation, it is important to understand abnormal returns. A stock’s actual return represents its real market performance during a given period, while the expected return estimates how the stock should have performed under normal market conditions. The abnormal return is simply the difference between these two values. Positive abnormal returns indicate that the stock outperformed expectations, while negative abnormal returns suggest weaker-than-expected performance. Identifying abnormal returns accurately is the first step because cumulative abnormal return depends entirely on combining these individual daily differences across the chosen event period.

Why Cumulative Abnormal Return Calculation Is Important

Cumulative abnormal return calculation provides valuable insights into how financial markets react to significant corporate or economic events. Investors use it to evaluate whether announcements such as mergers, dividend changes, earnings reports, or leadership transitions created value for shareholders. Researchers rely on CAR when conducting event studies to understand market efficiency and investor behavior. Companies may also analyze cumulative abnormal returns to assess how strategic decisions influence stock performance. Because it separates expected market movement from event-driven changes, this method offers a clearer picture of how specific news affects investor confidence and market valuation over time.

Key Components Required for CAR Analysis

Accurate cumulative abnormal return calculation depends on several essential components. Analysts first identify the event date that may influence stock prices. Next, they select an estimation window to determine expected returns and an event window to observe market reactions before and after the event. Actual stock returns and market index returns are then collected from reliable financial data sources. Using an appropriate financial model, expected returns are estimated and compared with actual performance to calculate abnormal returns. These daily abnormal returns are then accumulated to produce the final cumulative abnormal return value for analysis.

How Cumulative Abnormal Return Calculation Works

The cumulative abnormal return calculation process follows a logical sequence that helps analysts evaluate market reactions systematically. First, expected returns are estimated using a recognized financial model, such as the market model or capital asset pricing approach. Next, actual stock returns during the event window are collected and compared with expected values to identify abnormal returns. Finally, all abnormal returns within the selected event period are added together to produce the cumulative abnormal return. A positive CAR suggests the event generated favorable investor reactions, while a negative CAR indicates the market responded less positively than anticipated.

Common Applications in Financial Research

Cumulative abnormal return calculation plays an important role in academic research and professional financial analysis. Universities frequently use CAR in event studies to examine how markets respond to corporate announcements, government policies, or economic shocks. Investment firms analyze cumulative abnormal returns to evaluate acquisition strategies, executive appointments, stock buybacks, and product launches. Financial consultants also apply this technique when advising clients about investment performance around major events. Because it measures value creation beyond normal market expectations, CAR remains one of the most respected analytical tools for understanding stock price behavior in modern financial markets.

Factors That Can Influence CAR Results

Several factors can affect the accuracy and interpretation of cumulative abnormal return calculation. The selection of the event window significantly influences results because market reactions may occur before or after the official announcement. Choosing an appropriate estimation period is equally important for generating reliable expected returns. Market volatility, unexpected economic news, industry trends, and investor sentiment may also impact stock performance independently of the event being studied. Analysts must carefully control these variables to ensure cumulative abnormal returns reflect the actual influence of the targeted event rather than unrelated market movements or external conditions.

Best Practices for Accurate Cumulative Abnormal Return Calculation

Producing reliable cumulative abnormal return calculation results requires careful planning and sound analytical methods. Analysts should use high-quality financial data, define event dates precisely, and select estimation and event windows that align with research objectives. Applying consistent financial models and testing statistical significance strengthen the credibility of findings. It is also important to consider market conditions that may influence stock prices independently of the event. Thorough documentation and transparent methodology improve the reliability of both academic and professional studies. Following these best practices helps generate meaningful conclusions that support informed investment and research decisions.

Conclusion

Cumulative abnormal return calculation is a valuable financial technique that measures how specific events influence stock performance beyond normal market expectations. By comparing actual returns with expected returns and combining abnormal returns over a defined period, analysts gain deeper insights into investor reactions and value creation. Whether used in academic research, corporate finance, or investment analysis, CAR provides an effective way to evaluate the true impact of important events. Understanding its principles, calculation process, and practical applications enables investors and researchers to make better-informed decisions while improving the quality and accuracy of financial analysis.